September 13, 2024

When a buyer uses an FHA loan, the home needs to meet some basic standards before the sale can close. In simple terms, the property has to be safe to live in, have working essential systems and be in overall livable condition. These requirements help the lender approve the loan.

This guide breaks down what FHA inspections actually look for, the issues that most often slow sellers down, when there may be some flexibility and what options you have if making repairs isn’t realistic.

What is an FHA Inspection?

An FHA inspection is part of the FHA appraisal and confirms the home meets HUD’s minimum safety, security and habitability standards. A HUD-approved appraiser looks at the property’s condition alongside its value to make sure the home is safe to live in and acceptable for an FHA-backed loan. This review focuses on whether the home meets FHA’s basic requirements at the time of sale, not cosmetic issues or long-term maintenance concerns.

If the appraiser spots issues that don’t meet FHA standards, those items are flagged as required repairs. The loan can’t move forward until those issues are corrected and verified, which may involve follow-up paperwork or a return visit from the appraiser.

Is an FHA Inspection the Same as a Home Inspection?

An FHA inspection is not a full home inspection. It focuses on visible issues that affect safety, structural stability and basic functionality, rather than cosmetic details or future maintenance issues a private inspector might note. The appraiser doesn’t test every system in depth or provide the kind of detailed report a licensed home inspector would.

Because of this limited scope, many buyers still choose to order a separate home inspection for their own peace of mind. From a seller’s perspective, this matters because FHA-required repairs are limited to safety and livability concerns, not everything that might appear on a private inspection report.

Why Does FHA Require Property Condition Standards?

FHA loans are federally insured through the U.S. Department of Housing and Urban Development. HUD sets basic property standards to reduce risk and make sure buyers are purchasing homes that are safe, sanitary and structurally sound at the time of sale. These standards are meant to prevent serious safety issues from delaying move-in or creating problems shortly after closing.

For sellers, this can feel stricter than conventional financing, especially when visible condition issues are involved, even if the home would otherwise sell without trouble.

Who Performs the FHA Inspection?

A HUD-approved appraiser conducts the inspection as part of the appraisal process. The appraiser reviews the home’s condition, notes any issues and documents required repairs on the Uniform Residential Appraisal Report, which is then sent to the lender.

If repairs are required, the appraiser may need to return to confirm they were completed before the loan can be approved. Until that confirmation happens, the closing timeline is usually paused.

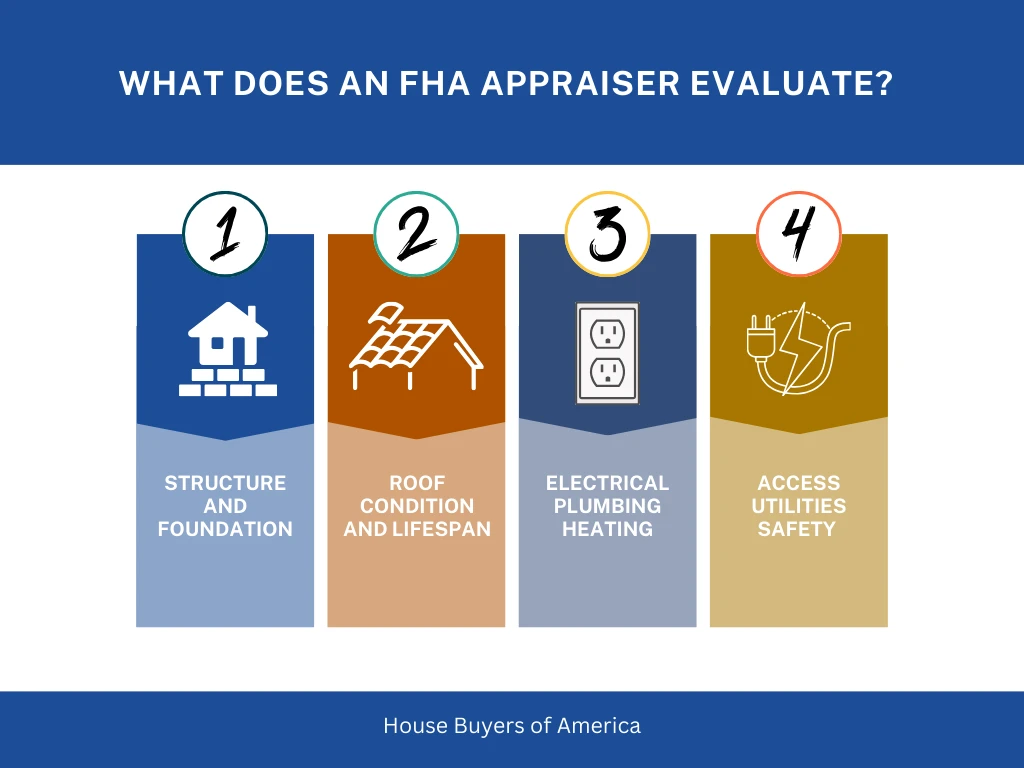

What Does an FHA Appraiser Evaluate?

An FHA appraiser evaluates the home’s value and whether it meets basic safety and habitability standards. This includes reviewing recent comparable sales to confirm the price makes sense while also looking at the home’s physical condition.

During the visit, the appraiser typically checks:

- The home’s structure and foundation

- Roofing condition and remaining life

- Electrical, plumbing and heating systems

- Access, utilities and basic safety features

The goal is to confirm the home is safe to live in and likely to hold its value. If issues are found, the loan stays on hold until those concerns are resolved through repairs or changes to the deal.

What Condition Issues Most Commonly Fail FHA Inspections?

Most FHA inspection issues come down to a few basics, like safety, structure or whether the home’s main systems are working properly. These are the kinds of problems that affect whether someone can safely live in the home right away, not cosmetic flaws or everyday wear and tear. FHA inspections focus on visible issues that could cause real problems if they’re left unaddressed.

For sellers, this usually means that bigger, more obvious issues are more likely to come up. Many of them are fairly easy to spot ahead of time, which can help you decide whether it’s worth making repairs or if another selling option might be a better fit.

1. Does the Roof Meet FHA Standards?

The roof must keep moisture out and have sufficient remaining life. Active leaks, severe damage or excessive roofing layers often trigger required repairs or replacement before approval.

2. Is the Structure Stable and Secure?

The home must be structurally sound and safe for occupancy. Large foundation cracks, rotting wood, termite damage, dampness or visible instability can stop loan approval until addressed.

3. Are Electrical, Plumbing and Heating Systems Functional?

All utilities must work safely and reliably. Exposed wiring, unsafe electrical panels, non-working plumbing or the absence of a permanent heat source commonly cause FHA delays.

4. Are There Health or Environmental Hazards?

The property must not pose health risks. This may include mold, lead-based paint in homes built before 1978, asbestos concerns or pest infestations that affect safety.

Can Location Cause an FHA Inspection Failure?

Yes. Location-related risks can affect FHA approval regardless of the home’s condition. Even if the house itself is in good shape, certain nearby factors can raise concerns during the FHA inspection. Properties near hazardous sites or exposed to ongoing disturbances may fail inspection because those risks can affect safety or long-term livability.

Examples include:

- Proximity to hazardous waste areas

- Nearby petroleum pipelines or areas with explosion risk

- Excessive noise from airports or industrial operations

These issues are less common, but when they come up, they’re usually outside a seller’s control and difficult to fix.

What Access Requirements Must FHA Homes Meet?

The property must be accessible year-round. FHA guidelines require that emergency vehicles, delivery services and everyday traffic can reach the home safely in all weather conditions. The site should not be isolated, landlocked or routinely affected by flooding.

For sellers, this usually comes into play with rural properties, shared driveways or homes located in areas that become difficult to reach during heavy rain or snow.

What Happens if the FHA Inspection Identifies Problems?

The loan does not close until required issues are corrected. When problems are found, the appraiser documents them, and the lender will pause the loan until those items are addressed. This can extend the timeline, especially if repairs take time or require follow-up inspections.

Once repairs are completed, proof is typically required before final approval is issued. Until then, the sale remains on hold.

Who is Responsible for FHA-Required Repairs?

Responsibility depends on how the sale is negotiated. FHA guidelines require that repairs be completed, but they do not specify whether the buyer or seller must pay for them. That decision is worked out as part of the purchase agreement.

In many cases, sellers cover repairs to keep the deal moving, but there are situations where costs are shared or handled differently depending on the agreement.

What Options Do Sellers Have When Repairs Are Required?

Sellers can make repairs, negotiate costs, offer credits or sell the home As-Is. The right choice depends on how extensive the repairs are, how quickly you need to close and whether FHA financing still makes sense for your situation. Each option comes with tradeoffs in terms of time, cost and certainty.

Should Sellers Make the Required Repairs?

Making repairs allows the FHA loan to proceed. This option tends to work best when the issues are minor, reasonably priced and won’t delay the closing significantly. For many sellers, fixing a few items is easier than starting over with a new buyer. However, larger or unexpected repairs can quickly change the math.

Can Sellers Negotiate Repair Responsibility?

Sellers and buyers may negotiate shared costs or price adjustments. In some cases, buyers are willing to take on repairs in exchange for a lower price or closing credits, as long as FHA requirements are still met. This approach can help keep the deal intact without putting the full burden on the seller.

Can Sellers Offer Repair Credits Instead?

Repair credits at closing allow the buyer to handle repairs after purchase. This can be a practical solution when repairs are straightforward but timing is tight. Credits keep the sale moving while avoiding construction delays before closing. It’s important to note that FHA-required repairs still need to be completed before the loan is approved.

When Does Selling As-Is Make More Sense?

Selling As-Is often makes sense when repairs are extensive, timelines are tight or FHA financing repeatedly falls through. In those situations, continuing to pursue FHA buyers can lead to repeated inspections, new repair requests and longer closing timelines, even when the home is priced fairly.

This option is often considered when repair costs start to outweigh the benefit of a higher sale price, or when making fixes would delay a move, tie up cash or add stress to an already complicated situation. Homes with older roofs, aging systems or deferred maintenance are more likely to run into these issues during FHA inspections.

Cash buyers are not bound by FHA inspection requirements and typically purchase homes in their current condition. Because there’s no lender approval involved, sales can move more quickly and with fewer last-minute surprises, offering a faster and more predictable path to closing when certainty matters most.

Are There Exceptions to FHA Inspection Rules?

Some requirements allow limited flexibility based on property type, location or climate. For example, certain features that are common in one region may be treated differently in another, especially when weather or local building norms are a factor. In some cases, alternative solutions may be acceptable if they still meet the intent of FHA guidelines.

However, safety and habitability standards are rarely waived. Issues that affect whether the home is safe to live in, such as structural problems, unsafe electrical systems or serious health risks, almost always need to be addressed before the loan can move forward.

What Should Sellers Do Before Accepting an FHA Offer?

Preparation reduces surprises and renegotiation. Taking a little time to look over the property before accepting an FHA-backed offer can help avoid delays later and make it easier to decide whether FHA financing makes sense for your situation.

Sellers should:

- Review roofing, utilities and access points early

- Address visible safety concerns

- Understand which repairs FHA commonly requires

- Decide whether FHA financing fits their goals

Doing this upfront puts you in a better position to move the sale forward with fewer last-minute decisions or changes.

Frequently Asked Questions About FHA Inspections

These are some of the most common questions people ask about FHA inspections and requirements.

- Do FHA inspections always require repairs?

FHA inspections only require repairs when safety, habitability or structural standards are not met. - Can buyers waive FHA inspection repairs?

Buyers cannot waive FHA-required repairs because the loan will not be approved until issues are resolved. - Does an FHA inspection affect the appraisal value?

An FHA inspection can affect appraisal value when condition issues impact approval or market valuation. - Can a seller refuse FHA repairs?

A seller can refuse to make FHA-required repairs, but the FHA loan will not close unless the issues are resolved or the deal changes. - How long is an FHA inspection valid?

An FHA inspection is typically valid for several months, but lenders may require an update if the closing is delayed or the property condition changes. - Can a seller sell a home As-Is with an FHA loan?

A seller can sell a home As-Is, but the property must still meet FHA minimum standards for the loan to close. - What repairs does FHA require sellers to fix most often?

FHA most often requires repairs related to safety, structural integrity, roofing, electrical systems and heating. - Can FHA inspection issues be negotiated with the buyer?

FHA inspection issues can be negotiated, but required repairs must be completed before loan approval, regardless of who pays.

What Are Your Next Steps as a Seller?

If your home meets FHA standards, financing may proceed smoothly. In that case, the inspection process is usually just another step toward closing, with few surprises along the way. As long as any minor issues are handled quickly, you can stay on track.

If repairs are significant, expensive or time-sensitive, selling As-Is to a cash buyer can eliminate inspection delays entirely. This approach avoids required repairs, repeated inspections and financing uncertainty.

If you’re looking for a faster, more predictable option, House Buyers of America works with homeowners who want to sell As-Is. They buy homes without FHA inspections, repair negotiations or financing contingencies, which can make it easier to move forward on your timeline.

Recent Posts

Frequently Asked Questions (FAQs) About Selling Your Home Fast

During a transfer, a new deed is drafted and signed by the seller, transferring ownership of the house to the new buyer. This document is then recorded in the land records with the above-mentioned deed of trust.

We work with your bankruptcy attorney to present a FAIR offer and give you additional money at closing. We present the offer directly to your attorney and work to have the offer accepted by the bankruptcy court. Once the offer is accepted, we ensure that the bankruptcy is released and we buy the property as soon as possible.

Yes, we can work with any seller who needs to move a property quickly for any reason and in any price range. We have purchased million-dollar houses before.

Yes, we buy apartments, multi-family houses/buildings and land.

No! You have no obligation at all if you submit an information form, show your property to House Buyers or receive an offer to buy your house. You are under no obligation at all. All we ask for is the opportunity to make an offer for your house, you’re in the driver’s seat as to whether you accept the offer or not. You are in complete control. You are only obligated to our service if you have entered into a purchase agreement with us, as with any other real estate transaction.

We need very basic information from you about your house. The number of bedrooms, bathrooms and overall condition of the property is needed. We will also ask you how long you have owned your home and if there are any mortgages or liens against the property.

We offer the maximum amount possible, our offers are very competitive. If our offers weren’t competitive, we wouldn’t have purchased thousands of houses! There is no magic percentage we use, every house is unique. Our Real Estate Consultants take into consideration the age, condition, size, features and location of the home much like an appraiser would. We factor in the costs to repair the house, what other homes in the area are selling for and how long it is taking to sell those homes. These and several other factors are researched to determine a fair offer.

As soon as we receive your Online Form, we will review your information and get back to you ASAP (usually within 30-60 minutes depending on when you submit the information).

We work FAST to help ensure that your house doesn’t go to foreclosure. We present you with a FAIR offer to pay off your mortgage before the foreclosure. We help save your credit, avoid foreclosure and allow you to sell your house FAST and FAIR. Due to recent legislation, if you reside in the state of Maryland and are within a certain period of time before your foreclosure sale date, we will introduce you to a Foreclosure Consultant. The legislation mandates that if you are within this certain window that a foreclosure consultant must explain to you all of your options involved in selling your home.

No problem! We can still buy your house as is, even if it has demolition orders scheduled.

Searching and Processing Address