January 6, 2025

Can you sell your home after refinancing?

Refinancing can be a smart way for homeowners to secure better mortgage terms, lower monthly payments, or access their home’s equity. But what if you decide to sell afterward? While it’s entirely possible, there are a few important things to consider—like financial implications, contract rules, and the current market.

This guide breaks down everything you need to know about selling your home after refinancing. We’ll cover key topics like breakeven points, owner-occupancy clauses, prepayment penalties, and even alternatives to refinancing, so you can make the best decision for your situation.

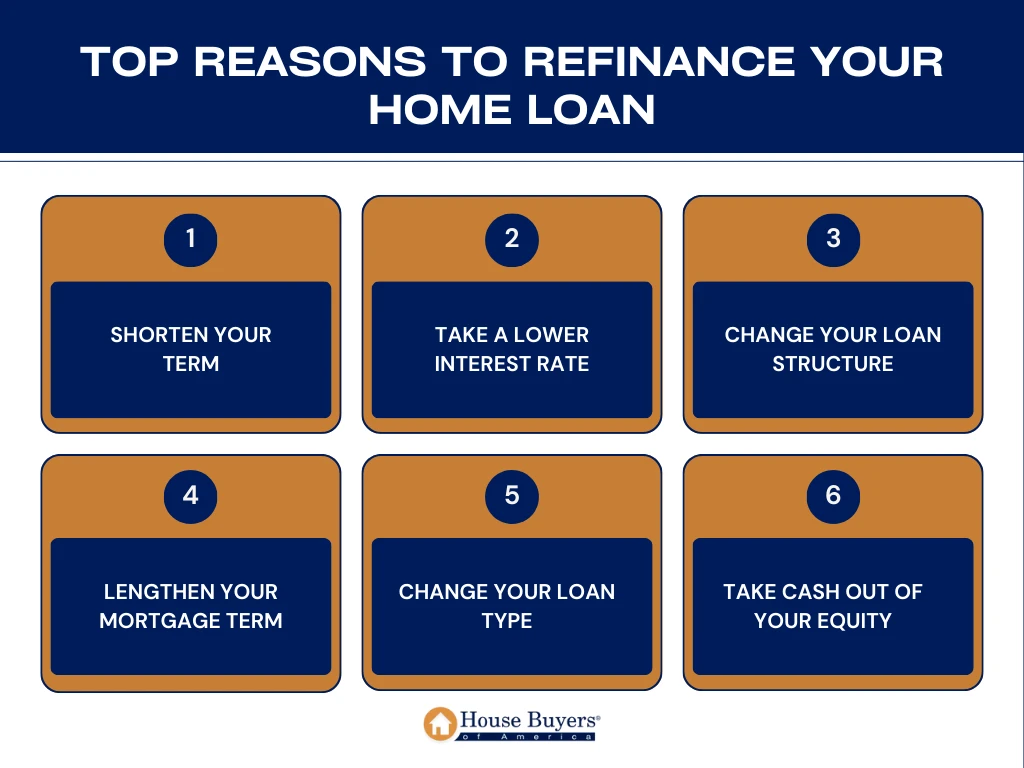

Top Reasons to Refinance Your Home Loan

Refinancing means replacing your current mortgage with a new one, usually with better terms. Homeowners often choose to refinance for a variety of reasons, depending on their financial goals and the current market conditions.

1. Shorten Your Term

By refinancing to a shorter loan term, you can pay off your mortgage faster and save thousands in interest. For example, refinancing a 30-year mortgage to a 15-year term can significantly reduce the overall cost of borrowing.

- Benefits:

- Faster homeownership.

- Significant interest savings.

- Considerations:

- Monthly payments may increase, so ensure your budget can accommodate the higher cost.

2. Take a Lower Interest Rate

Lowering your interest rate through refinancing can reduce your monthly payments and overall loan costs. This is especially beneficial when interest rates drop or your credit score improves.

- Example: If you refinance a $250,000 loan from 5% APR to 3.5%, you could save over $100,000 in interest over the life of the loan.

3. Change Your Loan Structure

Switching from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage can provide financial stability by eliminating the risk of fluctuating interest rates.

- Who Benefits?

- Homeowners who prefer predictable payments.

- Those anticipating rising interest rates.

4. Lengthen Your Mortgage Term

If you’re struggling with high monthly payments, refinancing to a longer term can provide relief. For instance, moving from a 15-year to a 30-year term reduces monthly payments but increases the overall interest paid.

- Key Consideration: Use this option as a short-term solution, as the long-term costs can outweigh the benefits.

5. Change Your Loan Type

Refinancing from a government-backed loan (e.g., FHA) to a conventional loan can eliminate mortgage insurance once you reach 20% equity.

- FHA Example: Refinancing an FHA loan with 3.5% down to a conventional loan can save you thousands by avoiding lifetime mortgage insurance premiums.

6. Take Cash Out of Your Equity

A cash-out refinance allows you to borrow against your home’s equity, providing funds for renovations, debt consolidation, or other expenses.

- Use Cases:

- Home improvements to boost resale value.

- Paying off high-interest debt.

How Soon Can You Sell Your Home After Refinancing?

Selling your home after refinancing is possible, but timing is critical. Factors like breakeven points, contractual clauses, and market conditions influence whether selling soon after refinancing makes sense.

Breakeven Point

The breakeven point is when your savings from refinancing equal the costs of the refinance. Selling before reaching this point often results in financial loss.

- Calculation Example:

-

- Refinance Costs: $8,000

- Monthly Savings: $200

- Breakeven Point: $8,000 ÷ $200 = 40 months (3.3 years)

-

If you sell before hitting this mark, you may not recover your refinancing costs.

Owner-Occupancy Clauses

Many refinance contracts include owner-occupancy clauses requiring you to live in the home as your primary residence for a specified period, often 12 months. Violating this clause can lead to legal and financial consequences.

- Advice: Always review your refinance agreement for occupancy requirements. Contact your lender for clarification if needed.

Is There a Penalty for Selling Your Home After Refinancing?

Prepayment penalties are fees charged when you pay off your mortgage early, typically within the first few years of the loan term.

- Types of Prepayment Penalties:

-

- Hard Penalty: Applies to both selling and refinancing.

- Soft Penalty: Only applies to refinancing.

-

Check your loan terms to determine if these penalties apply.

How Long After a Cash-Out Refinance Can You Sell Your House?

Selling after a cash-out refinance is possible but often discouraged unless absolutely necessary. Prepayment penalties, loss of equity, and increased loan balances are significant considerations.

How Long Can You Stay in Your House After Refinancing?

The length of time you stay in your home after refinancing affects whether the refinance is financially beneficial. Several factors influence this decision:

Breakeven Point

As mentioned earlier, the breakeven point is a key metric. Staying beyond this period ensures that your refinance savings outweigh the costs.

Financial Planning Considerations

- Short-Term: Refinancing with plans to sell within two years often results in financial loss due to upfront costs.

- Long-Term: Refinancing makes more sense if you plan to stay in your home for at least 5–7 years.

Personal Circumstances

Life events, such as job relocations or family changes, may necessitate selling your home sooner than planned. In such cases, weigh the financial implications carefully.

What Happens If I Back Out of a Refinance Before Closing?

Backing out of a refinance before closing is sometimes the right decision, especially if unexpected changes make the refinance no longer beneficial. However, it’s important to understand the potential consequences and costs associated with this choice to avoid surprises.

Why Might You Back Out of a Refinance?

There are several reasons homeowners decide not to proceed with refinancing:

- Unfavorable Terms: If the final terms differ significantly from the initial offer—such as higher interest rates or additional fees—you may decide it’s not worth it.

- Change in Financial Goals: Personal circumstances, like an unexpected job loss, a need to sell the home sooner than planned, or a major expense, may alter your priorities.

- Better Options Elsewhere: After starting the refinance process, you may find a different lender offering a more competitive deal.

- Market Conditions: A sudden change in interest rates or home values may make the refinance less beneficial.

Potential Costs of Backing Out

While you can typically cancel a refinance before signing the final paperwork, certain fees may not be refundable. These include:

- Application Fees: Many lenders charge upfront fees to process your application, which often cannot be recovered if you back out.

- Appraisal Fees: If your lender has already ordered an appraisal of your home, you are responsible for this cost, regardless of whether you proceed.

- Credit Check Fees: If a hard inquiry has already been run on your credit, it will remain on your credit report even if you decide not to refinance.

How to Minimize Costs When Backing Out

- Understand Your Contract: Before beginning the refinancing process, review your agreement for information about refundable and non-refundable fees.

- Communicate Early: If you know you’re backing out, inform your lender as soon as possible to avoid additional services (e.g., title search, underwriting) that may add to your costs.

- Shop Around Before Committing: To avoid backing out, compare offers and terms from multiple lenders before submitting an application.

Key Considerations Before Starting the Process

- Evaluate Your Financial Goals: Ensure the refinance aligns with your long-term goals. For example, if you’re planning to sell your home soon, refinancing might not make sense.

- Ask Questions: Discuss potential fees and penalties for backing out with your lender upfront, so you’re fully aware of the financial implications.

- Have a Contingency Plan: Life is unpredictable, so build flexibility into your financial strategy. If your circumstances change mid-process, reassess whether refinancing is still the best move.

When Backing Out May Save You Money

Walking away from a refinance might cost you some fees upfront, but it can save you from a long-term financial mistake. For example:

- If you discover hidden costs or unfavorable terms, backing out prevents locking yourself into a disadvantageous loan.

- If your situation changes and you no longer plan to stay in the home long enough to recoup refinancing costs, it’s better to cancel early.

Advice for Moving Forward

If you’re reconsidering a refinance:

- Revisit Your Financial Priorities: Ensure that refinancing still aligns with your current and future goals.

- Discuss Concerns with Your Lender: Some lenders may adjust terms to keep you from backing out, such as waiving certain fees or offering more competitive rates.

- Explore Alternatives: If refinancing no longer makes sense, consider options like a loan modification, HELOC, or cash-out refinance.

By understanding the potential costs and benefits of backing out, you can make an informed decision that protects your financial health.

Do You Lose Equity If You Refinance?

Refinancing typically doesn’t reduce your equity in a straightforward way, but certain factors can indirectly impact the amount of equity you retain in your home. Understanding how refinancing interacts with your home equity is key to making informed financial decisions.

How Refinancing Affects Equity

When you refinance, you replace your existing mortgage with a new one. The process itself doesn’t remove equity from your home; the equity remains based on the difference between your home’s market value and your loan balance. However, specific refinancing actions and associated costs can influence your equity in the following ways:

Cash-Out Refinances: Borrowing Against Your Equity

A cash-out refinance is a type of refinancing where you take out a larger loan than your current mortgage balance and receive the difference as cash. This directly reduces your equity because you’re converting some of it into loan debt.

- Example:

- Before Refinancing: Your home is valued at $300,000, and you owe $200,000, leaving you with $100,000 in equity.

- After a Cash-Out Refinance: You refinance for $250,000, taking $50,000 in cash. Your equity now decreases to $50,000 (assuming no additional appreciation in value).

While this reduces equity, it can be a strategic move for funding renovations, consolidating debt, or covering large expenses—provided the benefits outweigh the costs.

- Considerations:

- Ensure you don’t borrow more than necessary, as it increases your debt and monthly payments.

- Understand the risks if property values decrease, potentially leaving you with less equity than the loan balance.

Closing Costs and Their Impact

Even for standard (non-cash-out) refinancing, closing costs can indirectly reduce your equity if they’re rolled into the new loan balance instead of paid upfront.

- Example:

- Your current mortgage balance is $200,000.

- Refinancing closing costs are $6,000.

- If you roll these costs into your new loan, your mortgage balance becomes $206,000, reducing your equity.

Though the impact might seem small initially, rolling costs into your loan increases the principal you owe and the interest you pay over time, chipping away at your financial flexibility.

Market Value Considerations

Equity is tied to your home’s market value, so external factors can influence your equity post-refinance:

- Market Appreciation: If your home’s value increases significantly, it can offset reductions caused by a cash-out refinance or rolled closing costs.

- Market Depreciation: A decline in property values could shrink your equity, particularly if you recently refinanced for a higher balance.

How to Protect Your Equity During a Refinance

- Evaluate Loan Terms Carefully: Avoid borrowing more than necessary, and ensure refinancing aligns with your long-term goals.

- Pay Closing Costs Upfront: If possible, avoid rolling these costs into your loan balance to preserve equity.

- Maintain a Healthy Loan-to-Value (LTV) Ratio: Lenders often allow you to refinance up to 80% of your home’s value. Keeping your LTV lower helps retain equity and improves your financial position.

When Losing Equity Might Be Worth It

While reducing equity may seem undesirable, there are scenarios where it makes sense:

- Funding High-Value Projects: Using equity for home improvements can increase your property’s value, potentially rebuilding or even increasing equity.

- Debt Consolidation: Paying off high-interest debts with equity can save money in the long run, even if it temporarily reduces your stake in the home.

By understanding how refinancing decisions like cash-out refinances and rolled closing costs affect your equity, you can plan strategically to minimize negative impacts and maximize financial benefits.

Does It Really Make Sense to Refinance If You Plan to Sell the House in Less Than 2 Years?

Refinancing can be a powerful financial tool, but it may not always be the best choice—especially if you plan to sell your home within two years. In most cases, the costs and risks associated with refinancing outweigh the potential benefits in such a short timeframe. Here’s a closer look at why it’s generally not recommended and what alternatives you might consider.

Why Refinancing May Not Be Worth It for Short-Term Plans

- High Closing Costs

- Refinancing comes with significant upfront costs, typically ranging from 2% to 6% of the loan balance. For example, refinancing a $200,000 loan could cost between $4,000 and $12,000 in closing fees. These costs are only recovered over time, making it difficult to justify refinancing if you plan to sell quickly.

- Inability to Recoup Costs

- The breakeven point—the time it takes for monthly savings to cover refinancing costs—often takes several years. If you sell before reaching this point, you could end up losing money instead of saving it.

- Example: If refinancing saves you $150 per month but costs $6,000 in fees, it would take 40 months (over three years) to break even. Selling within two years means you would still be at a financial loss.

- Potential Prepayment Penalties

- Some refinance agreements include prepayment penalties, which are fees for paying off the loan early. If you sell shortly after refinancing, these penalties could add thousands of dollars to your costs, further reducing the financial viability of refinancing.

Alternatives to Refinancing for Short-Term Needs

If you plan to sell within two years, consider these alternatives instead of a traditional refinance:

- Loan Modification

- A loan modification allows you to adjust the terms of your existing mortgage without the need for refinancing. For instance:

- You might negotiate a lower interest rate.

- Your lender could extend your loan term to reduce monthly payments.

- This option typically has lower costs and can provide short-term relief without locking you into a new loan.

- A loan modification allows you to adjust the terms of your existing mortgage without the need for refinancing. For instance:

- Home Equity Line of Credit (HELOC)

- A HELOC lets you access your home’s equity without replacing your primary mortgage. It works like a credit card, giving you a revolving line of credit that you can use as needed.

- Advantages:

- Lower upfront costs compared to refinancing.

- Flexibility to borrow only what you need.

- Use Cases: HELOCs are ideal for funding home improvements or consolidating debt before selling, allowing you to boost your home’s value or reduce financial burdens.

- Wait to Refinance

- If refinancing still seems appealing, consider waiting until after you sell your home. This ensures you won’t be tied down by new loan terms, closing costs, or penalties when you’re ready to move.

When Refinancing Might Make Sense Despite Short-Term Plans

In rare cases, refinancing could still be a viable option, even if you plan to sell within two years:

- Market Conditions Favor It

- If interest rates are exceptionally low, refinancing could save enough in monthly payments to offset closing costs within a shorter timeframe.

- Cash-Out Refinance for Home Improvements

- If your home needs significant upgrades to maximize its selling price, a cash-out refinance could provide the funds to increase your property’s value. Just ensure the increased value outweighs the costs of refinancing.

- Rapid Market Appreciation

- In a booming real estate market, rising property values could offset refinancing costs, making it worthwhile to refinance and sell sooner.

Key Takeaways

- Refinancing is rarely a good idea if you plan to sell your home within two years due to high costs and short breakeven timelines.

- Alternatives like loan modifications or HELOCs often provide better short-term solutions without the financial downsides.

- In special cases, like rapid market appreciation or significant home upgrades, refinancing might still be worth considering.

By carefully weighing your options and understanding the potential costs, you can make a decision that aligns with your financial goals and timeline.

Alternatives to Selling After Refinancing

If selling your home after refinancing isn’t practical or financially feasible, you still have several options. These alternatives can help you make the most of your current situation while minimizing financial strain.

Loan Modification

A loan modification involves renegotiating the terms of your existing mortgage with your lender, typically without the need to refinance. This can be an excellent solution for homeowners facing financial difficulties or those needing temporary relief from high payments.

- How It Works:

- Your lender may lower your interest rate, extend the loan term, or adjust your monthly payments to make them more manageable.

- Some lenders may even agree to reduce the principal balance in rare cases.

- When to Consider It:

- If you’re struggling to meet your monthly payments due to changes in income or expenses.

- When refinancing isn’t an option due to credit issues or high costs.

- Advantages:

- Lower upfront costs compared to refinancing.

- Keeps your original mortgage in place, avoiding new closing costs.

- Considerations:

- Approval is at the lender’s discretion, and not all requests are granted.

- Loan modifications can sometimes impact your credit score.

No-Closing-Cost Refinance

A no-closing-cost refinance allows you to avoid paying upfront closing costs by rolling those expenses into the new loan’s principal or accepting a slightly higher interest rate. While this increases your overall loan balance or monthly payments, it eliminates the need for immediate out-of-pocket expenses.

- How It Works:

- Instead of paying thousands of dollars at closing, the costs are either added to your loan balance or offset by a higher interest rate.

- When to Consider It:

- If you need immediate cash flow but still want to refinance for better loan terms.

- If you plan to sell the home in the near future and want to avoid large upfront costs.

- Advantages:

- Preserves cash for other needs, such as home improvements or emergencies.

- Enables refinancing without the financial burden of closing costs.

- Considerations:

- A higher loan balance means you’ll pay more interest over time.

- Suitable for short-term strategies, but less ideal if you plan to stay in the home long-term.

Convert to an Investment Property

If selling your home isn’t viable, converting it into a rental property can provide a steady income stream while covering your mortgage payments. This option is particularly useful if you’ve moved to a new location but don’t want to sell your former residence.

- How It Works:

- You rent out your home to tenants, using the rental income to cover your mortgage and other property-related expenses.

- Hiring a property manager can help if you don’t want to handle the day-to-day responsibilities of being a landlord.

- When to Consider It:

- If you’re in a strong rental market and can generate sufficient income to cover costs.

- When selling your home would result in financial loss due to low equity or market conditions.

- Advantages:

- Generates passive income while allowing you to hold onto the property.

- Gives you time to wait for the market to improve before selling.

- Considerations:

- You’ll need to ensure the home complies with local rental regulations.

- Managing tenants and property maintenance can be time-consuming.

- Your lender may require you to notify them if the home is no longer your primary residence.

By exploring these alternatives, you can find a solution that aligns with your financial goals and personal circumstances, avoiding the need to sell your home after refinancing while still maintaining financial flexibility.

When Does It Make Sense to Sell After Refinancing?

Selling your home after refinancing can seem counterintuitive due to the associated costs and potential penalties. However, there are circumstances where selling after refinancing not only makes sense but could also be a strategic financial decision. Below are some scenarios where it might be the right move, along with considerations to keep in mind.

1. Market Appreciation

When home values rise rapidly, the equity gained from market appreciation can offset the costs of refinancing and selling.

- Example:

- You refinanced your home six months ago with $200,000 remaining on your loan balance.

- Since then, your home’s value has increased from $250,000 to $300,000 due to a hot real estate market.

- Even after paying closing costs and potential prepayment penalties, you still walk away with significant equity.

- When It Makes Sense:

- You’re in a seller’s market where demand is high, and homes are selling above asking price.

- The increase in your home’s value outweighs the costs of refinancing and selling.

- Key Consideration: Consult a real estate agent to determine how much you could net from the sale and whether it justifies the costs.

2. Life Changes

Unexpected personal or professional circumstances may require you to sell your home, regardless of whether you’ve recently refinanced.

- Common Scenarios:

- Job Relocation: A new job opportunity in another city or state necessitates a move.

- Family Needs: Expanding your family, downsizing after children move out, or accommodating an elderly relative.

- Divorce or Separation: A change in marital status may lead to the sale of jointly owned property.

- When It Makes Sense:

- The move is unavoidable, and holding onto the home as a rental property isn’t feasible.

- Selling helps you meet your new financial or personal goals more effectively.

- Key Consideration: Factor in any prepayment penalties or owner-occupancy clauses in your refinance agreement to avoid unexpected costs.

3. Reaching the Breakeven Point

The breakeven point is when the savings from refinancing equal the costs of refinancing. Selling after this point ensures you’ve recouped those costs and are no longer at a financial disadvantage.

- Example:

- You refinanced your mortgage to save $200 per month and paid $6,000 in closing costs.

- It took 30 months to reach the breakeven point. Selling after this period means the refinance no longer represents a financial loss.

- When It Makes Sense:

- You’ve stayed in the home long enough to recoup refinancing costs.

- Market conditions and your personal financial situation align to make selling advantageous.

- Key Consideration: Use a refinancing calculator to determine your breakeven point and ensure you’ve reached it before deciding to sell.

4. Major Repairs or Renovations Funded by Refinancing

If you used a cash-out refinance to fund home improvements, selling the home after completing those upgrades may make financial sense.

- Example:

- You refinanced to add a new kitchen or renovate the bathrooms, significantly increasing the home’s market value.

- The sale price after renovations exceeds the combined cost of refinancing and the improvements.

- When It Makes Sense:

- The renovations substantially increased your home’s resale value.

- The added value outweighs the costs of the refinance and sale.

- Key Consideration: Ensure the upgrades align with buyer preferences in your area to maximize returns.

5. Escaping Negative Equity or Financial Strain

In some cases, refinancing may have temporarily improved your financial situation, but selling is the only way to achieve long-term stability.

- Example:

- You refinanced to lower your monthly payments but now face rising expenses or an unexpected financial burden.

- Selling allows you to eliminate the mortgage entirely and reset your financial priorities.

- When It Makes Sense:

- Holding onto the property is no longer sustainable or aligns with your financial goals.

- You can sell without incurring significant penalties or losses.

Selling your home after refinancing isn’t always ideal, but there are situations where it’s the right move. If market conditions, life changes, or financial goals align, selling can help you maximize the benefits of your refinance and adapt to your evolving needs.

This section provides unique, valuable insights and should be included in the article, as it addresses common concerns homeowners face when considering a sale after refinancing. Expanding it with these detailed scenarios makes it even more helpful without redundancy.

Can You Refinance While Your Home Is Listed for Sale?

Refinancing a home that is actively listed for sale is generally challenging, as most lenders are hesitant to approve loans in such cases. However, there are exceptions and strategies that may allow you to refinance under specific conditions. Here’s a more detailed look at why refinancing while selling is difficult, the exceptions, and what to consider if you’re in this situation.

Why Lenders Are Reluctant to Approve Refinancing on Listed Homes

Lenders typically avoid refinancing homes that are listed for sale because:

- Increased Risk for Lenders: If a home is listed, the borrower is signaling an intent to sell, which increases the likelihood of the loan being paid off early. This means the lender may not collect enough interest to make the loan profitable.

- Owner-Occupancy Concerns: Many refinance agreements include owner-occupancy clauses requiring borrowers to live in the home for a set period, often 12 months. A home listed for sale suggests the borrower may not fulfill this requirement.

- Instability in Borrower Intent: Refinancing is often designed to provide long-term benefits, but a pending sale indicates short-term plans, which contradict the lender’s expectations.

Exceptions to the Rule

While refinancing an actively listed home is uncommon, certain scenarios may allow it:

- Delisting the Home

- If you remove your home from the market, some lenders may consider your refinance application. This signals that you intend to stay in the home, which aligns with typical refinance agreements.

- Key Consideration: Be prepared to meet owner-occupancy requirements, as lenders will expect proof of your intent to remain in the home.

- Investment Property Refinancing

- If you plan to convert the home into a rental property rather than selling it, certain lenders may offer refinancing options tailored to investment properties.

- Key Consideration: Investment property loans often come with stricter terms, higher interest rates, and larger down payment requirements.

- Cash-Out Refinance for Home Improvements

- If the purpose of the refinance is to fund upgrades that could boost the home’s market value, some lenders may approve the loan, especially if the home is temporarily delisted during the process.

- Key Consideration: Ensure that the added value from the improvements outweighs the costs of the refinance.

Steps to Take if You Want to Refinance a Listed Home

- Delist Your Home Temporarily

- If selling isn’t an urgent priority, delisting your home during the refinancing process can improve your chances of approval.

- Advice: Communicate with your real estate agent and lender to align timelines.

- Check Owner-Occupancy Requirements

- Review your refinance terms for clauses that specify how long you must live in the home post-refinance. Violating these clauses could lead to penalties or loan default.

- Work With Specialized Lenders

- Some lenders specialize in unique situations, such as refinancing homes that are listed for sale or properties intended for rental conversion. Explore options outside of traditional banks.

Alternative Options If Refinancing Isn’t Feasible

If refinancing isn’t possible while your home is listed, consider these alternatives:

- Home Equity Line of Credit (HELOC):

- A HELOC can provide access to your home’s equity without requiring a complete refinance. This is particularly useful if you need funds for upgrades or repairs to increase your home’s sale price.

- Bridge Loan:

- A bridge loan offers short-term financing that can cover expenses until your home sells. This is ideal for homeowners who need immediate cash but plan to pay it off quickly with proceeds from the sale.

- Sell First, Then Refinance:

- If refinancing isn’t viable, focus on completing the sale and then explore refinance options for your next property.

Key Considerations

- Timing Is Critical: If you’re determined to refinance while selling, carefully plan the timing to meet lender requirements while aligning with your selling strategy.

- Market Impact: In hot real estate markets, the urgency to sell might outweigh the benefits of refinancing. In slower markets, refinancing could provide more time to prepare for a better sale.

- Lender Communication: Be transparent with potential lenders about your plans to sell or delist. Open communication can help you find lenders willing to work within your unique circumstances.

While refinancing a home that is actively listed for sale is rarely approved, exceptions do exist. Delisting the home, exploring investment property refinancing, or considering alternative financial options can help you navigate this situation. Always evaluate your long-term goals and consult with financial and real estate professionals before proceeding.

This section is valuable and unique to the article, as it addresses a specific scenario that many homeowners may face. Expanding it with actionable advice and detailed considerations makes it even more informative.

Key Takeaways About Refinancing Before Selling Your Home

Refinancing before selling is a nuanced decision requiring careful planning and consideration of your financial goals. Understanding critical factors like breakeven points, prepayment penalties, and available alternatives can help you weigh the benefits and drawbacks of this choice. It’s essential to evaluate your timeline, current market conditions, and the costs involved to ensure that refinancing aligns with your overall strategy.

When in doubt, consult with a financial advisor or mortgage expert to explore personalized solutions and determine the best path forward for your unique situation. With the right guidance, you can make a confident decision that supports both your short- and long-term financial well-being.

Recent Posts

Frequently Asked Questions (FAQs) About Selling Your Home Fast

During a transfer, a new deed is drafted and signed by the seller, transferring ownership of the house to the new buyer. This document is then recorded in the land records with the above-mentioned deed of trust.

We work with your bankruptcy attorney to present a FAIR offer and give you additional money at closing. We present the offer directly to your attorney and work to have the offer accepted by the bankruptcy court. Once the offer is accepted, we ensure that the bankruptcy is released and we buy the property as soon as possible.

Yes, we can work with any seller who needs to move a property quickly for any reason and in any price range. We have purchased million-dollar houses before.

Yes, we buy apartments, multi-family houses/buildings and land.

No! You have no obligation at all if you submit an information form, show your property to House Buyers or receive an offer to buy your house. You are under no obligation at all. All we ask for is the opportunity to make an offer for your house, you’re in the driver’s seat as to whether you accept the offer or not. You are in complete control. You are only obligated to our service if you have entered into a purchase agreement with us, as with any other real estate transaction.

We need very basic information from you about your house. The number of bedrooms, bathrooms and overall condition of the property is needed. We will also ask you how long you have owned your home and if there are any mortgages or liens against the property.

We offer the maximum amount possible, our offers are very competitive. If our offers weren’t competitive, we wouldn’t have purchased thousands of houses! There is no magic percentage we use, every house is unique. Our Real Estate Consultants take into consideration the age, condition, size, features and location of the home much like an appraiser would. We factor in the costs to repair the house, what other homes in the area are selling for and how long it is taking to sell those homes. These and several other factors are researched to determine a fair offer.

As soon as we receive your Online Form, we will review your information and get back to you ASAP (usually within 30-60 minutes depending on when you submit the information).

We work FAST to help ensure that your house doesn’t go to foreclosure. We present you with a FAIR offer to pay off your mortgage before the foreclosure. We help save your credit, avoid foreclosure and allow you to sell your house FAST and FAIR. Due to recent legislation, if you reside in the state of Maryland and are within a certain period of time before your foreclosure sale date, we will introduce you to a Foreclosure Consultant. The legislation mandates that if you are within this certain window that a foreclosure consultant must explain to you all of your options involved in selling your home.

No problem! We can still buy your house as is, even if it has demolition orders scheduled.

Searching and Processing Address