December 19, 2025

Asbestos is one of the most common concerns homeowners face when selling older properties. Because it’s associated with serious health risks, many sellers worry that asbestos automatically makes a home unsafe, legally risky, or impossible to sell. Others assume they’ll be required to remove it before listing or fear buyers will walk away once it’s disclosed.

In reality, asbestos is a well-known issue in residential real estate, particularly in homes built before the 1980s. Selling a house with asbestos is legal, common, and often far less complicated than homeowners expect. What matters most is what the seller knows, how that information is disclosed, and whether the asbestos is intact or damaged.

Having a basic understanding of the rules, buyer expectations, and available options can save sellers time, money, and frustration during the sale.

What Asbestos Is and Why It Still Exists in Residential Homes

Asbestos is a naturally occurring mineral composed of microscopic fibers that resist heat, fire, and chemical damage. For much of the 20th century, it was widely used in residential construction because it strengthened materials and improved insulation and fire resistance.

As a result, asbestos can still be found in many homes built before the late 1970s, including in:

- Floor tiles and adhesives

- Ceiling texture and acoustic finishes

- Pipe, boiler, and furnace insulation

- Roofing shingles and siding

- Wall and attic insulation

Asbestos is not considered dangerous simply because it exists in a home. The health risks arise when asbestos-containing materials deteriorate or are disturbed, allowing fibers to become airborne and inhaled. Long-term exposure to airborne asbestos fibers has been linked to serious illnesses, including asbestosis, lung cancer, and mesothelioma, often appearing decades after exposure.

Because intact asbestos can remain stable for many years, many homes contain asbestos without posing an immediate health threat.

Is It Legal to Sell a House With Asbestos?

Yes, it is legal to sell a house with asbestos since there is no federal law that prohibits doing so. Sellers are not required under federal law to remove asbestos before selling, nor are they generally required to test for it.

However, asbestos is regulated at both the federal and state level, primarily through disclosure and safety rules, not sale restrictions. Federal laws such as the Toxic Substances Control Act regulate asbestos use and handling but do not ban the sale of homes where asbestos is present.

State laws play a much larger role in real estate transactions. Most states require sellers to disclose known material defects or environmental hazards. Once a seller has actual knowledge of asbestos – through testing, inspections, or past remediation – that information typically must be disclosed to potential buyers.

Disclosure rules differ by state, with some requiring sellers to disclose known asbestos outright and others focusing on whether it creates a hazard. Others require disclosure only if the asbestos creates a safety issue or has caused damage. Because these requirements differ, sellers should review state-specific disclosure forms carefully and seek guidance if needed.

Selling a home As-Is does not eliminate the duty to disclose known asbestos. An As-Is sale simply means the seller is not agreeing to make repairs, not that they can withhold material information.

Seller Disclosure Obligations and Legal Risk

Disclosure is one of the most important aspects of selling a home with asbestos. Most states require sellers to complete a property disclosure statement identifying known defects or hazards. When asbestos is known to be present, sellers are generally expected to disclose:

- That asbestos-containing materials exist

- Where those materials are located, if known

- Any testing, inspection, or remediation history

- Whether asbestos has been removed, sealed, or left in place

If a seller isn’t sure whether asbestos is present, disclosure forms usually allow them to note that the condition is unknown rather than guess. Problems tend to arise only when known asbestos isn’t shared with buyers, which can lead to disputes later over who should cover removal or related costs. Being upfront about what you know helps set expectations early and lowers the chances of issues surfacing after the sale is complete.

Is Asbestos Testing Required Before Selling a House?

In most cases, sellers are not legally required to test their home for asbestos before putting it on the market. Federal authorities such as the U.S. Environmental Protection Agency (EPA) make it clear that federal law does not mandate that residential sellers disclose or test for asbestos in typical home sales, although state or local rules can require disclosure if known.

Many sales move forward without testing, especially when an older home is well maintained and no renovations are planned. In homes built before the late 1980s, asbestos is often assumed in certain materials, but that alone doesn’t require testing.

Some sellers choose to test to reduce uncertainty. While inspectors can flag materials that appear to contain asbestos, only lab testing can confirm it. Testing costs vary, and once asbestos is confirmed, that information may need to be disclosed to buyers.

Testing can provide clarity, but it also comes with added disclosure considerations, which is why many sellers weigh the benefits before deciding to move forward.

Do Sellers Have to Remove or Abate Asbestos Before Selling?

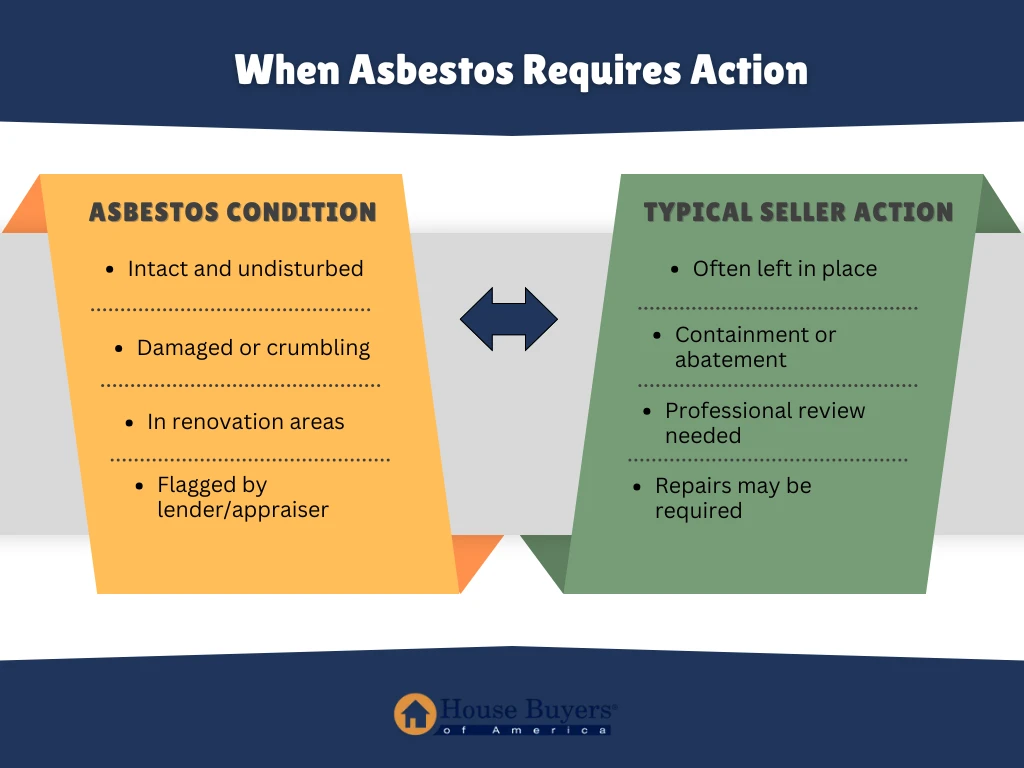

In most situations, sellers do not have to remove or abate asbestos before selling a home. When asbestos-containing materials are in good condition and not being disturbed, many homes are sold with those materials left in place.

Public health agencies often caution against unnecessary removal. Disturbing asbestos can release fibers into the air, which can create more risk than leaving stable materials alone. For that reason, keeping asbestos in place is often considered the safer option when it’s intact and not causing problems.

Removal or professional containment typically comes into the conversation when asbestos is:

- Visibly damaged, crumbling, or breaking down

- Located in areas where repairs or renovations are likely

- Flagged during an inspection or appraisal as a potential safety concern

When sellers do decide to address asbestos, they generally choose between two approaches. Containment involves sealing or covering the material so fibers can’t escape and is often the less disruptive, lower-cost option when materials are stable. Full abatement removes the asbestos entirely but requires more time, coordination, and expense. The right choice usually depends on the condition of the material, how the home will be used, and how the sale is expected to unfold.

How Asbestos Affects Pricing, Negotiations, and Buyer Decisions

Asbestos doesn’t usually stop a home sale on its own, but it often becomes part of the conversation once inspections begin. For most buyers, it’s less about panic and more about understanding what they’re taking on and how it might affect future costs or plans for the home.

When asbestos comes up, buyers commonly respond in a few practical ways:

- Asking for a price adjustment to reflect potential future work

- Requesting a closing credit so they can handle containment or removal after the sale

- Wanting documentation that shows the asbestos is intact or has already been addressed

In many cases, a credit at closing is easier to work with than lowering the list price. Credits give buyers flexibility to deal with asbestos on their own timeline, while sellers avoid reopening broader pricing negotiations or resetting expectations for appraisers and other buyers.

Asbestos can also shape who shows interest in the home. Some buyers are comfortable moving forward, especially in older neighborhoods where asbestos is common and well understood. Others may hesitate, particularly if they plan to remodel areas where asbestos is present or want to avoid additional projects after moving in.

Financing and Appraisal Considerations

When asbestos comes up during a home sale, financing issues usually relate to condition rather than presence. Many lenders will finance homes that contain asbestos as long as the material is intact, not exposed, and not creating an immediate health or safety concern. In those cases, asbestos is often treated as a known feature of an older home rather than a defect that stops the deal.

The appraisal is usually where asbestos enters the financing conversation. Appraisers are not testing for asbestos, but they are required to note visible conditions that could affect livability or value. Issues are more likely to be flagged when asbestos-containing materials are damaged, crumbling, or located in areas where they’re likely to be disturbed.

How different loan types typically respond

Financing outcomes often depend on the type of loan involved:

- Conventional loans – These are generally the most flexible. If asbestos is stable and not visibly deteriorating, conventional financing often moves forward without additional requirements.

- Government-backed or more conservative loan programs – These programs tend to apply stricter health and safety standards. If damaged or exposed asbestos is identified, repairs or professional containment may be required before closing.

What happens if a lender requires action

If asbestos becomes a condition of financing, sellers and buyers usually have a few paths forward:

- The seller completes containment or abatement before closing

- The buyer accepts a credit and completes the work after closing, if allowed by the loan

- The parties renegotiate pricing or terms to reflect the added work

Any of these options can add time and coordination to the transaction, especially when licensed asbestos contractors are involved.

When cash buyers become more appealing

If financing requirements start to slow things down, cash buyers and investors often remain an option. Because they aren’t subject to lender repair rules, they can purchase homes with asbestos As-Is, even when materials are damaged. While cash offers may come in lower, they can reduce uncertainty and help sellers avoid delays tied to loan approvals.

Common Seller Strategies and How to Prepare Before Listing

When asbestos is present, there isn’t a single right way to handle the sale. Most sellers choose an approach based on the condition of the material, how competitive the local market is, and how much time or flexibility they have. The goal is usually the same: reduce friction during negotiations and avoid surprises once the home is under contract.

Sellers typically take one of the following paths:

- Sell the home with asbestos disclosed and left in place

- Offer a credit at closing instead of completing remediation

- Complete professional containment or abatement before listing

- Sell the home As-Is to a cash buyer or investor

Whichever strategy makes sense, preparation plays a big role in keeping the transaction on track. Before listing, sellers should gather any asbestos-related documentation they have, such as testing results, inspection notes, or records of prior containment or removal. Avoid disturbing suspected asbestos materials, as that can create unnecessary risk and complicate the sale.

Disclosure forms should be completed carefully and accurately, reflecting only what is known rather than assumptions. If there’s uncertainty about what needs to be disclosed, a real estate professional or attorney familiar with local requirements can help clarify expectations and reduce the chance of disputes later.

Taken together, strategy and preparation help sellers manage asbestos as part of the transaction, rather than letting it become an obstacle that derails the sale.

Can You Sell a House With Asbestos?

Yes, you can sell a house with asbestos, and it happens every day. Asbestos on its own doesn’t make a home unsellable or illegal to transfer. What matters is understanding what you know about the property, disclosing that information appropriately, and choosing a selling approach that fits your timeline and comfort level.

For some sellers, that means listing traditionally and negotiating credits or pricing. For others, especially when repairs, testing, or financing hurdles feel like too much, a faster As-Is sale makes more sense. With the right expectations and a clear plan, asbestos becomes one factor in the transaction, not the thing that stops it.

If you’d rather avoid inspections, repairs, or extended negotiations altogether, House Buyers of America offers homeowners a straightforward option. They purchase homes As-Is, including properties with asbestos concerns, and provide cash offers with flexible closing timelines. It’s a practical path for sellers who want certainty, speed, and fewer moving parts when selling an older home.

Recent Posts

Frequently Asked Questions (FAQs) About Selling Your Home Fast

During a transfer, a new deed is drafted and signed by the seller, transferring ownership of the house to the new buyer. This document is then recorded in the land records with the above-mentioned deed of trust.

We work with your bankruptcy attorney to present a FAIR offer and give you additional money at closing. We present the offer directly to your attorney and work to have the offer accepted by the bankruptcy court. Once the offer is accepted, we ensure that the bankruptcy is released and we buy the property as soon as possible.

Yes, we can work with any seller who needs to move a property quickly for any reason and in any price range. We have purchased million-dollar houses before.

Yes, we buy apartments, multi-family houses/buildings and land.

No! You have no obligation at all if you submit an information form, show your property to House Buyers or receive an offer to buy your house. You are under no obligation at all. All we ask for is the opportunity to make an offer for your house, you’re in the driver’s seat as to whether you accept the offer or not. You are in complete control. You are only obligated to our service if you have entered into a purchase agreement with us, as with any other real estate transaction.

We need very basic information from you about your house. The number of bedrooms, bathrooms and overall condition of the property is needed. We will also ask you how long you have owned your home and if there are any mortgages or liens against the property.

We offer the maximum amount possible, our offers are very competitive. If our offers weren’t competitive, we wouldn’t have purchased thousands of houses! There is no magic percentage we use, every house is unique. Our Real Estate Consultants take into consideration the age, condition, size, features and location of the home much like an appraiser would. We factor in the costs to repair the house, what other homes in the area are selling for and how long it is taking to sell those homes. These and several other factors are researched to determine a fair offer.

As soon as we receive your Online Form, we will review your information and get back to you ASAP (usually within 30-60 minutes depending on when you submit the information).

We work FAST to help ensure that your house doesn’t go to foreclosure. We present you with a FAIR offer to pay off your mortgage before the foreclosure. We help save your credit, avoid foreclosure and allow you to sell your house FAST and FAIR. Due to recent legislation, if you reside in the state of Maryland and are within a certain period of time before your foreclosure sale date, we will introduce you to a Foreclosure Consultant. The legislation mandates that if you are within this certain window that a foreclosure consultant must explain to you all of your options involved in selling your home.

No problem! We can still buy your house as is, even if it has demolition orders scheduled.

Searching and Processing Address